A few years ago, the rules for how companies report leases on their financial books changed with something called IFRS 16. The main goal was to be more honest about a company's true financial commitments.

Why the change?

Before, it was pretty easy for companies to sign big lease deals for things like buildings or equipment and keep those big commitments hidden off their main financial report (the balance sheet). IFRS 16 stopped this. Now, for lessees, almost all leases have to be shown directly on the balance sheet, giving everyone a clearer picture of what a company really owes.

For companies that lease assets (Lessees)

- No more hiding: If you lease equipment, office space, etc., almost all those leases now show up on your balance sheet as a “right of use asset" and a "lease liability”.

- Service vs. Lease: Contracts that are purely for services usually stay off the balance sheet - as long as they don’t involve control of a specific asset.

- Some flexibility, limited impact: Structuring payments to be variable or short-term can sometimes limit the balance sheet impact. But remember, economic substance always overrides the legal form of a lease..

For companies that lease assets out (Lessors)

While IFRS 16 brought big changes for lessees, lessor accounting remains largely unchanged.

- Finance vs. operating lease: Lessors still classify leases as either:

- Finance leases (where most risks and rewards of ownership are transferred), or

- Operating leases (where they are not).

- Finance leases (where most risks and rewards of ownership are transferred), or

- Revenue timing: In a finance lease, a lessor recognizes revenue and profit upfront. In an operating lease, income is recognized over time.

- It’s not a choice: Whether a lease qualifies as a finance lease depends on objective criteria, not what the company prefers.

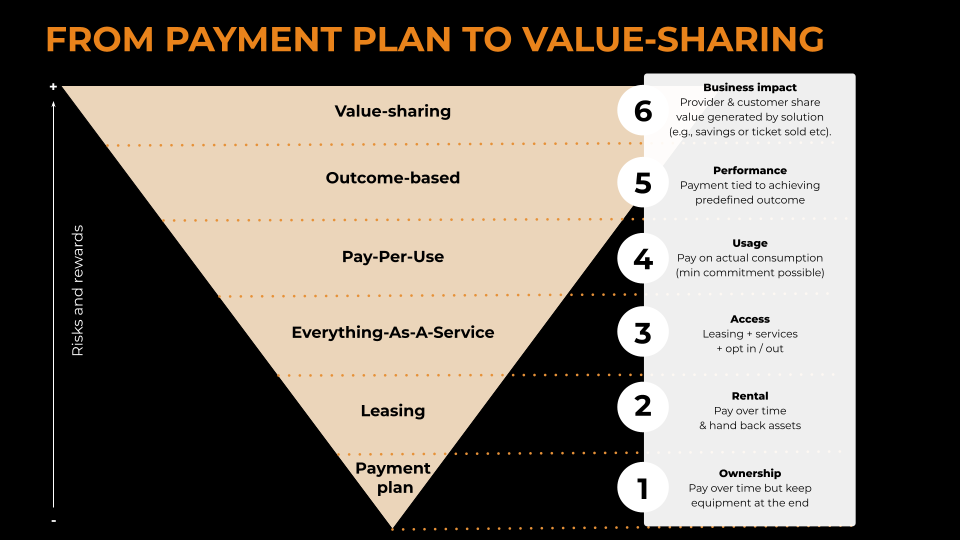

"As-A-Service" deals

- In standard service contracts, revenue is recognized over time, as the service is delivered. But, if your "As-a-Service" deal actually includes the use of a dedicated equipment (e.g., hardware bundled into a managed service), this may contain an embedded lease.

- In that case, the equipment portion may need to be accounted for separately under IFRS 16, which could accelerate some revenue recognition depending on the structure.

What the auditor says...

- Auditors may disagree on how specific contracts should be treated, especially in complex hybrid contracts.

- What matters most is substance over form: what’s actually happening in the contract, not just how it’s written.

- Always work closely with your auditor to ensure alignment.

In short:

- Most leases now appear on the books, especially for lessees.

- Lessor accounting hasn’t changed much, but classification still affects revenue timing.

- As-A-Service models require careful analysis under both IFRS 16 and IFRS 15.

- Auditor judgment matters so align early to avoid surprises.

Fast track compliance

Confused by these complex financing rules?

At Black Winch, we make it simple. We will help you fast-track revenue and margin recognition for your As-A-Service and leasing contracts.

Book a FREE 30-minute session with our finance expert, Sophie Feret, today! Click here to book your call.

Disclaimer

This content is for informational purposes only and does not constitute accounting, tax, or legal advice. Readers should consult with their own professional advisors before making decisions based on this material. The interpretation of IFRS standards may vary depending on individual circumstances and auditor judgment.