Equipment prices are rising fast across sectors. Memory, components, energy, logistics, raw materials… everything is under pressure.

The impact is simple: customers still need the equipment but they hesitate longer. They delay CAPEX approvals. They negotiate harder. Deals slow down.

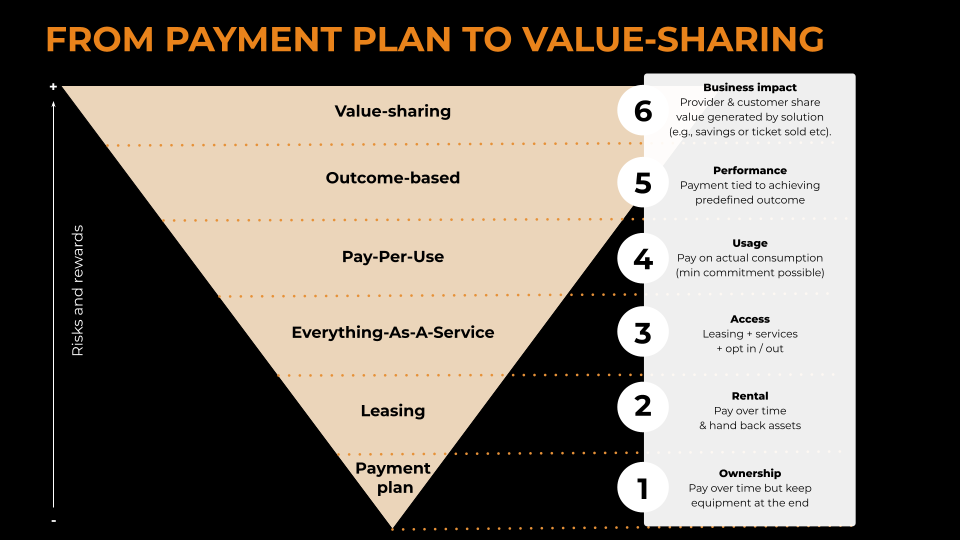

In this context, the question is no longer whether to move to As-A-Service.

The real question is: how fast can you do it?

For manufacturers, there are only two viable paths:

- If you don’t yet have a structured As-A-Service offer, you need to launch one fast.

- If you already have one, you need to scale it fast.

Because in a market where prices are rising structurally, speed of execution is now a competitive advantage.

A cross-sector cost surge

IT and Digital Infrastructure

In IT specifically, memory prices are no longer following traditional cyclical patterns. Analysts warn that server memory prices could ultimately double by late 2026 compared to early 2025, largely because production is being shifted toward high-bandwidth memory for AI workloads rather than commodity modules.

Major OEMs have already indicated strong pricing pressure across their server portfolios, with anticipated double-digit percentage increases on certain product lines as component costs rise.

These are not marginal adjustments. When memory and core components increase this sharply, the total cost of servers and infrastructure changes significantly. The result is a familiar pattern: customers still need the equipment, but they hesitate longer, they negotiate harder, and they delay CAPEX approvals.

Industrial Equipment

Industrial equipment is also exposed, even when the products are not “digital” in the traditional sense. Machines and production lines increasingly rely on electronics, sensors, embedded systems, and automation components. At the same time, manufacturers face inflation in raw materials, energy costs, and logistics.

In many industrial segments, equipment price increases of 5–15% are becoming common. For end customers, that is often enough to trigger a freeze in capital decisions, especially for mid-market companies.

Medical Equipment

Healthcare equipment is one of the most structurally constrained markets. Medical devices, imaging systems, and diagnostic platforms are sensitive to electronics supply chains and component inflation. However, hospitals operate under strict budgets, long procurement cycles, and political approval processes.

Global health spending trends show medical costs, including equipment, services and technology adoption, continuing to rise by around 10% per year on average across regions.

This combination makes CAPEX purchasing difficult even when the equipment is essential. It also makes subscription, pay-per-use, or service-based access models far more attractive than they used to be.

Energy and Sustainability Equipment

The transition to cleaner energy has increased demand for EV charging stations, solar power arrays and battery storage solutions. These systems often combine electronics with heavy infrastructure components. Rising pricing for control systems, power electronics and installation labour are keeping total project costs high.

After a period of rock-bottom pricing, global costs for solar modules and energy storage equipment are now forecast to rise by about 9% heading into 2026, reflecting supply-side and policy shifts that end deep discounting.

Buyers still want the technology, but higher upfront costs mean longer deliberation and slower procurement cycles.

Mobility and Heavy Equipment

Construction machinery, agricultural vehicles, industrial trucks and marine systems are among the most capital-intensive categories.

Recent industry surveys show that around 34-50% of equipment managers reported price increases due to tariffs and broader cost pressures in 2025, with many seeing prices rise faster than general inflation.

When equipment prices increase by even a few percentage points, the absolute cost impact can be tens or hundreds of thousands of euros per unit.

This increases friction in purchase decisions, leading buyers to extend asset lifetimes or delay upgrades.

Premium Consumer Technology

Premium consumer technology categories such as gaming hardware, high-end audio systems and smart home devices are also affected. Spot and contract pricing for memory and storage has surged in 2025, with some NAND memory, a type of non-volatile storage technology that can retain data without a power source, spot prices tripling in short periods according to industry trackers.

These cost increases feed through to higher retail device pricing, which dampens consumer demand in price-sensitive segments.

How As-A-Service solves the cost challenge

When equipment costs rise, traditional CAPEX selling creates hesitation because buyers must commit a large sum of cash upfront.

As-A-Service models convert that payment into predictable operational spending. This allows buyers to preserve cash, reduce risk and move ahead with critical investments without waiting for lengthy capital approvals.

In this way As-A-Service helps unlock demand that would otherwise be stalled by rising prices and tighter budgets.

Two strategic options for manufacturers

Option 1: Launch an As-A-Service offer in 90 days

For companies that do not yet have a structured XaaS or leasing offer, the priority is speed. Waiting another year to “get it right” is risky because the market is already shifting.

With Black Winch, manufacturers can launch a bankable As-A-Service offer in 90 days, built to be commercially attractive, financially viable, and ready to scale.

The work focuses on the essentials:

- Designing pricing and segmentation that reflect current cost structures

- Structuring funding and finance partnerships that can underwrite subscription deals

- Building contracts and operational frameworks to support recurring revenue

- Preparing go-to-market assets and training sales teams to sell the model

By 1 June 2026, the objective is to have a bankable offer that sales teams and partners can sell with confidence.

Option 2: Scale in 60 days

If you already have an As-A-Service offer, the priority is not to redesign it. The priority is acceleration through your distribution network.

In most organisations, the offer exists but remains underused because distributors and resellers are not ready to sell it. They fall back on traditional hardware deals because it feels easier, faster, and more familiar. Until the channel can sell As-A-Service confidently, the model cannot grow.

With Black Winch, this scaling can be done in 60 days. We help you accelerate adoption across your distributor ecosystem so that resellers know how to position the offer, explain the financial logic, and sell it consistently.

Platforms like ComPaaS, our AI-powered CPQ for XaaS, equips resellers to automate configuration, pricing, quoting, and renewals for XaaS solutions, boosting retention.

The objective is simple. By 1 May 2026, your reseller network is ready to sell your As-A-Service offer at scale.

Conclusion:

The market is not waiting.

If equipment price inflation is already slowing your sales cycles, now is the time to act.

Launch your As-A-Service offer in 90 days. Or scale your existing one in 60.

At Black Winch, we build bankable, fundable and scalable As-A-Service models fast.

Let’s make sure rising prices accelerate your transition, instead of slowing your growth.

Contact us to define your 60- or 90-day roadmap.